Buying a house in 2022: How to get your offer accepted!

Yes, we are in a crazy real estate market & if you are planning on buying a home in 2022; you will need a strategy. Here are 5 things you need to consider to help get your offer accepted.

Have a strong escrow deposit.

First, what is an escrow deposit? This is money you put up with your accepted offer/contract. You are telling the seller I am a serious buyer and I will follow the terms of this contract to purchase your property. If I do not follow the terms of the contract; this money will be yours. If you do follow the terms of the contract, this money will be put towards your down payment at closing.

Depending on where you live, the escrow deposit is also known as earnest money or a good faith deposit. They all mean the same thing.

Your escrow deposit needs to be as strong as possible. In this market, a $1,000 escrow will not cut it. Even a 1%-2% of the purchase price might not be strong enough to help your offer stand out. It is not uncommon in this market to see a $10,000 escrow deposit on a $350,000 purchase. I recommend putting in as much as possible. Remember, this money will go towards your down payment at closing.

Shorten your inspection period

The Florida FAR/BAR AS IS contract is the common sales contract used in our area. The default time for an inspection is 15 days. In a “normal” market the most common time used is not this default time of 15 days, but is a 10 day inspection period. Our current market, the sellers & listing agents want this time as little as possible…5 to 7 days is the new normal with quite a few waiving an inspection altogether. I personally would never waive my inspection period because you really do not know the condition of the home. Since the average home sold in Brevard County was built in 1990, you are probably buying a home that is over 30 years old. If this is the case, you will need a 4 point inspection in order to obtain homeowners insurance. If you are paying cash, this isn’t as big of a deal because you can get some type of coverage while you do the repairs. If you are getting a mortgage you will need full coverage as a condition of the loan.

Offer a lease back

Sellers more than likely are looking for their next house or are waiting for their next house to close. Offering them post occupancy after your closing could help your offer stand out. They might need a couple days, a couple of weeks, or even a month to make this move. If you allow them this time to stay in the house it will have your offer stand out. Most sellers are also looking to have this post occupancy at no extra cost to them.

If you do allow the seller to stay in the house after closing, please talk to your insurance company about the right insurance coverage. More than likely you are buying the house to be your primary home which means the coverage you are getting is for you to live in the property. If something happens post occupancy with the seller still in the home; there is a good chance that the insurance company will deny the claim. The seller’s policy will not be in place after closing either…they might need to have a renters policy in place.

Appraisal Gap

In a perfect world, the sales contract price is what the appraisal comes in at. The lender is happy, you’re happy, everyone is happy. This market is far from that perfect world…Homes are listed above the comps. Offers are coming in well over the list price. This scenario makes an appraisal coming in at contract price almost impossible and appraisals are coming in low. Appraisal gaps are part of most contracts today because of this.

An appraisal gap in the offer is telling the seller IF the appraisal comes in under the contract price by $______ you are still moving forward with the purchase.

Here is an example to help understand what this means to you. In this example, you are under contract for $350,000 and are using a 20% downpayment ($70,000) and you are OK with a $25,000 appraisal gap.

The appraisal came in at $330,000 and the contract price is $350,000. There is a $20,000 difference/gap between the appraised value and the contract price.

Keep in mind that your loan is based upon the contract price BUT it is also based upon the appraisal price; which is $330,000. Your down payment is now $66,000. You also need $20,000 to cover the gap. You will need to bring $86,000 to closing plus your other closing costs.

If the appraisal gap is more than what is in the contract, you could pay the difference, see if the seller will adjust the price, or cancel the contract. Keep in mind this all has to happen within the timeframes of the financing contingency of the contract.

Something else to consider is talking with your lender about an appraisal waiver. I have seen scenarios where the buyer was putting 30% down that the lender and the option came up for the buyer to waive the appraisal.

If you really like living on the edge, you can simply remove the finance contingency altogether. This is something I would never recommend…

Seller closing costs

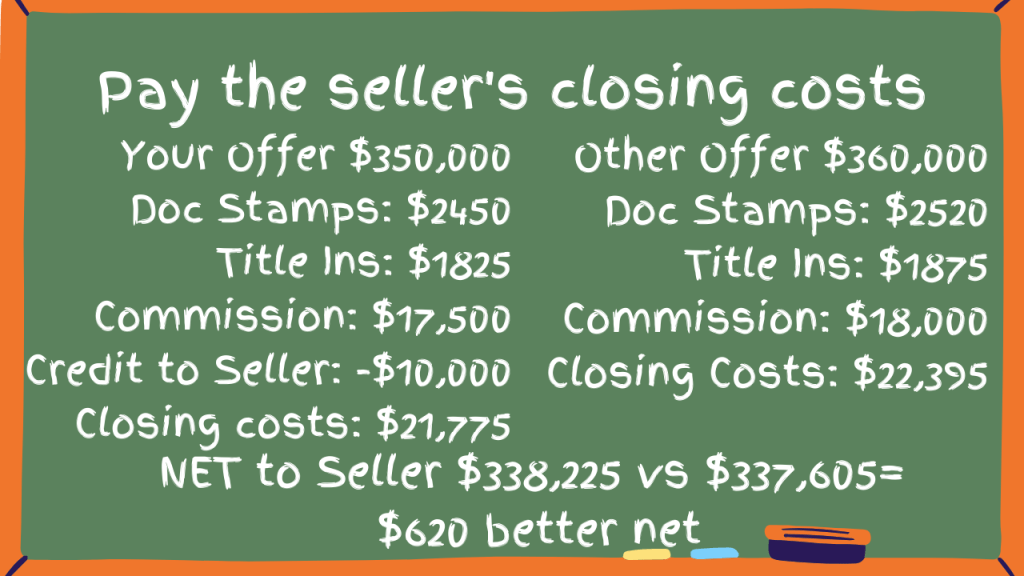

All the above scenarios are great ways to help your offer stand out. They are also becoming common on offers coming in. One thing that isn’t as common is offering to pay for the sellers closing costs. Both sides of the transaction will have their own closing costs to cover. The seller is responsible for title insurance, docs stamps on the deed, and the real estate commission with their closing costs. Based upon the $350,000 example, the seller will be paying $21,775 in closing costs. $1825 title insurance, $2450 doc stamps, $17,500 real estate commission(IF the real estate commission is 5%) If you offer to pay for all or some of this amount, your offer will definitely stand out. YES, this will add to your cash to close BUT this contribution will go directly to improving their bottom line. Here is what I mean. Instead of offering $360,000 offer $350,000 with $10K towards their closing costs.

Anytime the buyers I am working with use this scenario, I will include an estimated seller’s net sheet with the offer showing how it improves their bottom line and help get the offer accepted.

Using all of these suggestions or a combination of the 5 will help your offers stand out and get accepted. Planning on making a move in Cocoa Beach or Brevard County? I would love to help! You can access my calendar to schedule a call here https://calendly.com/eric_larkin or leave a message below.

Eric Larkin is a Broker Associate with Real Broker, LLC. He lives, works, and plays in the Cocoa Beach area. If you have questions about moving or relocating to Cocoa Beach and the Space Coast, let me know! I get calls, texts, direct messages & comments on my posts every day about the real estate market and things that are happening in Cocoa Beach and the Space Coast that I love answering. Ask me your questions on moving, relocating here, or anything about the community. I am here to help. I have been helping buyers and sellers with their real estate needs since becoming a real estate agent in 2003. My focus is always on helping, answering your questions, and doing everything possible to make certain you have a smooth transaction from beginning to end.

Planning a move or have questions about our area? Eric Larkin with Real Broker, LLC can help! Schedule a call here https://www.ericlarkin.com/schedule-a-call

OR leave your info here and I will call you https://www.ericlarkin.com/contact-form